Irs Code Which States Hsa Funds Can Be Used for Family Members

Key takeaways

- An HSA is a tax-deductible savings account used in conjunction with an HSA-qualified high-deductible wellness program.

- Contribution limits for 2020 are $three,550 if your HDHP covers simply yourself, and $vii,100 if it covers at least one other family member (increasing to $3,600 and $vii,200 in 2021).

- You lot tin buy HDHPs through your state's exchange – or off-exchange.

- Under new IRS rules, HDHPs are allowed to cover COVID-xix testing and treatment pre-deductible.

- Coronavirus relief deed changed the rules to allow OTC medications and menstrual products to be purchased with HSA funds.

- IRS expands preventive intendance umbrella to include some chronic intendance treatments, allowing HDHPs to pay for them pre-deductible.

- You withdraw your HSA funds – with no taxes or penalties – to pay for qualified medical expenses.

- Through 2019, in that location was transitional relief for plans that covered male contraception before the deductible.

- Review of your HSA should be function of an almanac financial check-up.

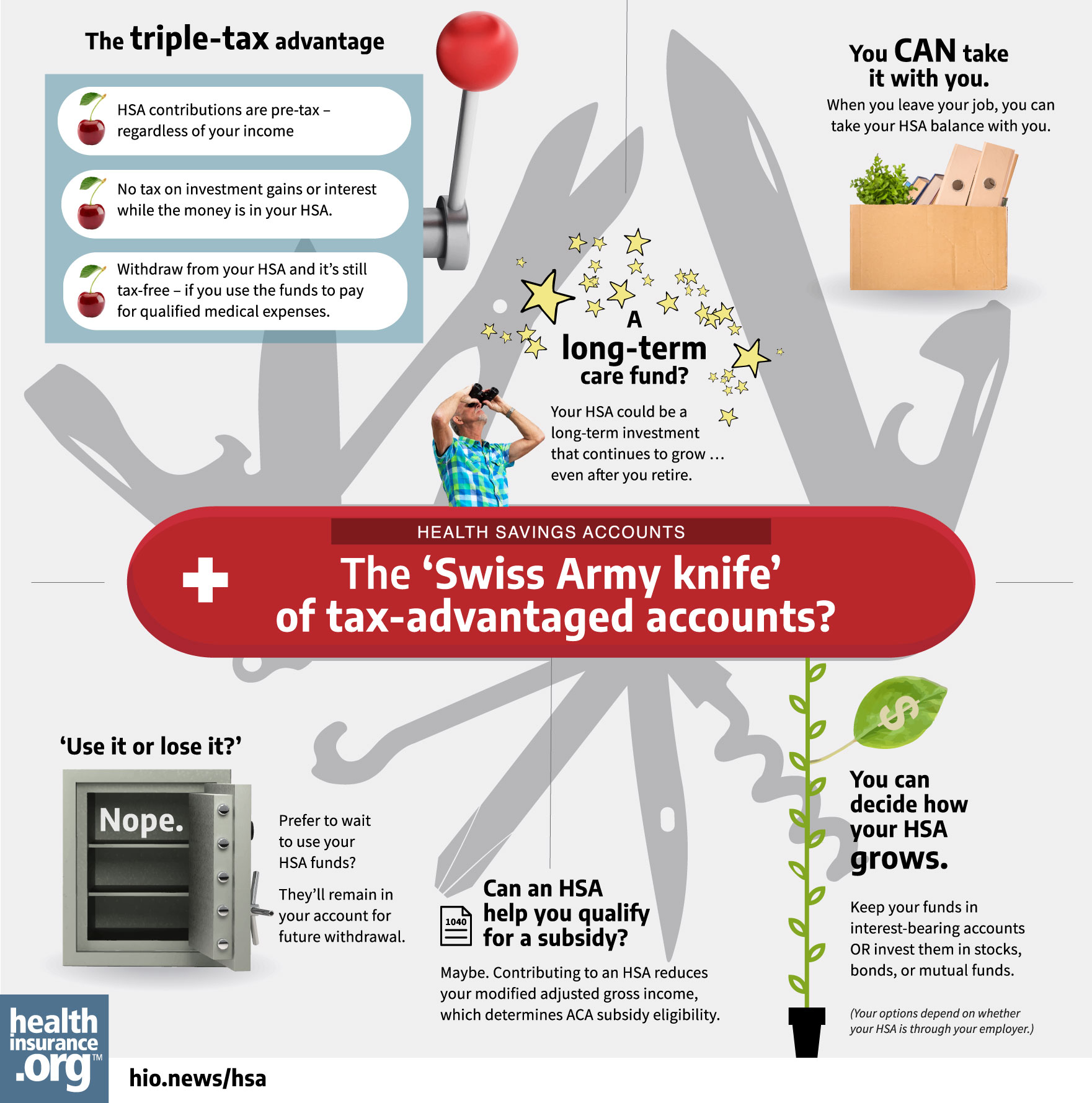

Infographic: The HSA: 'Swiss-Army knife' of tax-advantaged accounts?

A health savings account (HSA) is a tax-deductible savings account that'south used in conjunction with an HSA-qualified loftier-deductible health insurance plan (HDHP).

HSA contribution limits for 2020 and 2021

HSA regulations allow you to legally reduce federal income taxation past depositing pre-revenue enhancement money into a health savings account, as long every bit you lot're covered by an HSA-qualified HDHP. Only similar IRAs, HSA contributions can be made until April xv of the following year (for 2019 contributions, this was extended until July fifteen, 2020 due to the COVID pandemic).

For 2020, you tin can deposit up to $3,550 if you take HDHP coverage for just yourself, or $vii,100 if your HDHP covers at to the lowest degree 1 additional family fellow member. You have until Apr 15, 2021 to contribute some or all of this amount if you've got HDHP coverage in 2020.

For 2021, people with self-merely HDHP coverage can contribute upwards to $three,600 to an HSA, and those with family unit HDHP coverage can contribute upwardly to $7,200 ("family" coverage just ways that the HDHP covers at to the lowest degree i other family member; it does non have to embrace an entire family).

Account holders who are 55 or older are allowed to deposit an boosted $1,000 in catch-up contributions. (This amount is not adjusted for inflation; information technology's always $1,000.) HSA contributions tin can be made throughout the twelvemonth, or all at one time – it's upwardly to the account holder.

There'south no minimum deposit, but whatsoever you lot put into your business relationship is an "above-the-line" tax deduction that reduces your adapted gross income. If yous make your HSA contributions via your employer – as a payroll deduction – the money volition be taken out of your check before taxes, then you'll avoid both income taxation and payroll tax on the contributions.

The health plan that pairs with an HSA

Give yourself an 11-step financial check-up. Remember: You can make HSA deposits upwardly to the April 15 tax filing borderline.

Because the HSA is paired with a loftier-deductible health plan, your wellness insurance premiums will frequently be lower than they would be on a more traditional plan with a lower deductible. Merely HSA-qualified plans vary considerably in their out-of-pocket exposure; deductibles on HSA-qualified plans in 2021 tin can exist as low as $1,400 for an private and $ii,800 for a family unit.

So if you lot're buying your own wellness insurance (equally opposed to getting it from an employer), you'll observe them amongst Bronze, Silver, and even Gold plans, both on and off the exchange. And these plans are available near everywhere: For 2021, CMS reported that more than 99 percent of enrollees in states that apply HealthCare.gov would have admission to HSA-qualified health plans, upwards from 97 percent in 2020.

Simply since the maximum out-of-pocket limits on HSA-qualified plans are lower than the maximum commanded out-of-pocket limits on other plans (and the difference is growing with time), there will typically be some non-HSA-qualified plans (with higher out-of-pocket exposure) that accept lower premiums than the available HSA-qualified plans. So while an HSA-qualified plan volition typically exist among the lower-priced plans bachelor, information technology won't necessarily be the lowest-cost plan available.

Prior to 2016, information technology was common to meet HSA qualified plans that used aggregate family out-of-pocket limits. That meant the entire family unit out-of-pocket limit would demand to exist met before the plan'southward benefits kicked in, even if all the claims were for a single family member. Simply since 2016, all health plans – including HDHPs – must embed individual out-of-pocket maximums, which ways that no single family unit member'southward out-of-pocket expenses can exceed the individual out-of-pocket limit established past the ACA, even if the family is enrolled in an HDHP with a higher family out-of-pocket limit. (And this becomes more than important due to the aforementioned widening gap between the upper out-of-pocket limits immune for all plans under the ACA, versus the limit immune for HSA-qualified plans.)

Information technology'southward of import to note that you can only contribute to an HSA if your current wellness insurance policy is an HSA-qualified high-deductible wellness programme (HDHP). Not all plans with high deductibles are HSA-qualified, so cheque with your employer or your health insurance carrier if you're unsure. Contributions to your HSA can exist made past you or by your employer, and they're yours forever – in that location'south no "use it or lose information technology" provision with HSAs, and the money rolls over from 1 year to the adjacent. HSA funds can be stored in a diversity of savings vehicles, including banking concern accounts and brokerage accounts (ie, the funds tin be invested in the stock market if you prefer that pick and your HSA ambassador allows information technology), and there are numerous HSA custodians/administrators from which to choose.

IRS expands preventive care umbrella to cover some chronic intendance treatments

The ACA requires all not-grandfathered health plans to embrace preventive care before the deductible, and this provision applies to HDHPs as well. But under an HDHP, non-preventive services cannot be paid for by the health programme until the insured has met the deductible.

So HDHPs cannot have copays for role visits or prescriptions prior to the deductible existence met, which is one of the ways they differ from other health plans that have high deductibles but are not HDHPs.

But under new guidelines that the IRS issued in mid-2019, the list of preventive services that can be covered pre-deductible on an HDHP has been expanded to include certain treatments for certain specific chronic conditions. Information technology'southward optional for insurers to classify these services as preventive, merely if they do, the insurer can cover them (partially or in-full) earlier the enrollee meets the deductible, and the wellness plan volition continue to have its HDHP condition.

The atmospheric condition/treatments include:

- Congestive center failure or coronary artery affliction: ACE inhibitors and/or beta blockers

- Heart disease: Statins and LDL cholesterol testing

- Hypertension: Blood pressure monitor

- Diabetes: ACE inhibitors, insulin or other glucose-lowering agents, retinopathy screening, glucometer, hemoglobin A1c testing, and statins

- Asthma: Inhalers and peak period meters

- Osteoporosis or osteopenia: Anti-resorptive therapy

- Liver disease or bleeding disorders: International Normalized Ratio (INR) testing

- Low: Selective Serotonin Reuptake Inhibitors (SSRIs)

IRS allows HDHPs to pay for COVID-nineteen testing and treatment pre-deductible

With the exception of preventive care, HDHPs normally cannot pay for whatsoever medical services until the insured has met at least the minimum deductible set by the IRS. But in the face of the COVID-xix (coronavirus) pandemic, those rules have been relaxed. In March 2020, the IRS announced that HSA-qualified health plans would exist immune to pay for COVID-19 testing and treatment pre-deductible, without the wellness plan losing its HSA-qualified status.

The federal regime and numerous states are requiring health plans to cover COVID-xix testing with no cost-sharing, which ways the insured doesn't have to pay annihilation for the service. These rules apply to HDHPs just like any other plan, so the IRS announcement was important in terms of clarifying that people with HDHPs would all the same be able to contribute to HSAs in 2020, despite the fact that their health plans are now required to pay for an additional service (that isn't on the federally-divers list of preventive services) pre-deductible.

The federal government is non requiring health plans to cover COVID-19 treatment without cost-sharing, and neither are most states (New Mexico is, and Massachusetts is as long every bit the treatment is provided in a doctor'south function, urgent care clinic, or emergency room; state regulations don't apply to self-insured health plans). So HDHPs accept mostly had the choice to continue to require members to meet their normal cost-sharing requirements if they end up needing COVID-19 treatment (every bit opposed to just testing). Just if your HDHP does opt to suspend price-sharing for COVID-19 treatment (or to partially cover it pre-deductible), your plan will keep to be an HDHP and you'll all the same be able to contribute to an HSA for 2020.

CARES Act allows OTC medications and menstrual products to be purchased with HSA funds

As of 2011, the ACA prohibited the buy of over-the-counter medications with HSA funds, unless a doctor wrote a prescription for them. Only Section 4402 of the Coronavirus Aid, Relief, and Economic Security (CARES) Act changed that. The law, which was enacted in March 2020, eliminated the sentence at the stop of Department 223(d)(2) of the Internal Revenue Code of 1986 that had previously prohibited the purchase of non-prescription over-the-counter medications with HSA money (it used to say that qualified medical expenses "shall include an amount paid for medicine or a drug but if such medicine or drug is a prescribed drug (adamant without regard to whether such drug is bachelor without a prescription) or is insulin." That provision was eliminated under the CARES Deed)

Department 4402 of the CARES Human activity also changed the rules to allow menstrual products to be purchased with HSA funds.

Both of these changes are permanent and were retroactively effective to January one, 2020.

Using your HSA funds

You can use the taxation-free savings in your HSA to pay for doctor visits, infirmary costs, deductibles, co-pays, prescription drugs, or any other qualified medical expenses. Once the out-of-pocket maximum on your health insurance policy is met, your health insurance plan volition pay for your remaining covered medical expenses that year, the aforementioned as any other health plan.

If you lot switch to a health insurance policy that'southward non HSA-qualified, you'll no longer be able to contribute to your HSA, but you lot'll nevertheless be able to take money out of your HSA at any fourth dimension in your life to pay for qualified medical expenses, with no taxes or penalties assessed. If y'all don't utilise the money for medical expenses and still have funds available after age 65, you can withdraw them for non-medical purposes with no penalties, although income revenue enhancement would be assessed at that point, with the HSA functioning much like a traditional IRA.

Y'all tin can as well withdraw tax-free coin from your HSA to pay Medicare premiums (for Part A, if you have to pay premiums for it – although most people don't – and for Parts B and D, but not for Medigap plans). Tax-gratis HSA funds can also be used to pay long-term care premiums. There are limits on how much you can withdraw tax-gratis from your HSA to pay long-term care insurance premiums. (These limits are for 2020; the IRS indexes them for aggrandizement annually.) If your age is:

- 40 or younger, you can withdraw $430 taxation-free to pay long-term care insurance premiums

- 41 to 50, you can withdraw $810

- 51 to 60, you lot can withdraw $1,630

- 61 to 70, y'all can withdraw $4,350

- 71 or older, you lot can withdraw $v,430

IRS provided transitional relief for HSA-qualified plans that cover vasectomies and condoms before the deductible

While male contraception is non considered preventive care nether federal regulations (and thus coverage under a plan that covers male person contraception before the deductible would make a person ineligible to contribute money to an HSA), the IRS did not enforce that provision until 2020. So in 2018 and 2019, if you lot were in a state that required all plans to embrace male contraceptives before the deductible, y'all could still contribute to your HSA if yous had a plan that would otherwise have been considered HSA-qualified.

Here's the backstory on how this all works:

You can only contribute to an HSA while you're covered by an HSA-qualified HDHP. If you drop your wellness insurance coverage or switch to a non-HDHP, you have to end making HSA contributions.

1 of the requirements for a programme to be an HSA-qualified HDHP is that the program cannot pay for any services earlier the deductible, other than preventive care. Preventive care was defined by the IRS in Detect 2004-50, and that was revised in 2013 by Notice 2013-57, to clarify that any services deemed preventive care nether the ACA (and thus required to be covered on all not-grandfathered plans with no cost-sharing) would be considered preventive intendance for HSA-qualified plans too. That ensured that plans could be both ACA-compliant and HSA-qualified. (As noted in a higher place, it was further revised in 2019 to allow HSA-qualified plans to provide pre-deductible coverage for sure care for chronic conditions.)

But some states – including Illinois, Maryland, and Oregon – enacted laws requiring all state-regulated plans to cover FDA-approved contraceptives for men, earlier the deductible was met. Contraceptive coverage for women is considered preventive care under ACA regulations, so plans that cover female contraceptives earlier the deductible can still exist HSA-qualified. But male contraceptives are non considered preventive care under federal regulations.

So if a state requires all land-regulated plans (ie, all plans that aren't cocky-insured) to cover vasectomies and condoms at no cost — or in any class earlier the deductible is met — HSA-qualified plans in that state would terminate to be HSA-qualified.

In Maryland, the law requiring plans to fully comprehend male contraception took effect in Jan 2018, and concerns arose apace about the fact that people in Maryland with plans that were marketed as HSA-qualified would no longer be able to contribute to their HSAs, since their wellness plans were now providing pre-deductible benefits in backlog of what the IRS considers preventive intendance. Maryland enacted legislation in Apr 2018 to exempt HSA-qualified plans from the law that requires plans to cover male contraception, simply that wouldn't help people who had already purchased HSA-qualified plans for 2018.

In response to the puzzler faced by people who wanted HSA-qualified coverage in states requiring male person contraceptive coverage before the deductible, the IRS published Notice 2018-12. This notice clarifies that

- Male contraceptives are not considered preventive care nether federal guidelines, and then having a plan that covers them earlier the deductible would make a person ineligible to contribute to an HSA.

- The IRS is seeking comments on the preventive intendance rules for HDHPs, so it'south possible that IRS guidelines for allowable preventive intendance under an HSA-qualified plan could alter in the hereafter (but this has non happened as of 2020).

- Until the start of 2020, the IRS allowed people to contribute to an HSA even if their programme (which would otherwise be considered an HSA-qualified plan) covered male contraception before the deductible. This transitional relief also applied to plans that were issued before the IRS published Notice 2018-12, so a person who bought an otherwise-HSA-qualified plan for 2018 was immune to make the total twelvemonth HSA contribution for 2018.

The Illinois contraceptive mandate statute now also includes an exception for HDHPs [Sec 356z.4(iv)], and several other states have followed suit, issuing requirements that state-regulated wellness plans cover male person contraception, but with an exemption for HDHPs.

Louise Norris is an private health insurance banker who has been writing about health insurance and wellness reform since 2006. She has written dozens of opinions and educational pieces most the Affordable Care Human action for healthinsurance.org. Her land health commutation updates are regularly cited by media who cover health reform and by other health insurance experts.

stallingsfortainge.blogspot.com

Source: https://www.healthinsurance.org/glossary/health-savings-account/

0 Response to "Irs Code Which States Hsa Funds Can Be Used for Family Members"

Post a Comment